When Europe

established its 2020

objectives for the

energy transition

ten years ago, much of the debate

was focussed on the shift of energy

resources, away from polluting fossil

fuels towards cleaner renewable

alternatives.

When Europe

established its 2020

objectives for the

energy transition

ten years ago, much of the debate

was focussed on the shift of energy

resources, away from polluting fossil

fuels towards cleaner renewable

alternatives.

Only few would have

expected the entire sector, and its

prevalent business models, to change

so fast with it. In fact, when the Smart

Energy Demand Coalition, SEDC, set

out to establish the demand-side as

an interactive part of the energy value

chain, the system was characterised

by centralised supplies, delivered

uni-directionally to largely passive

consumers. Electricity, heating and

transport were separate sectors

with very little interaction. Today, it

is commonly accepted that the new

energy world is different.

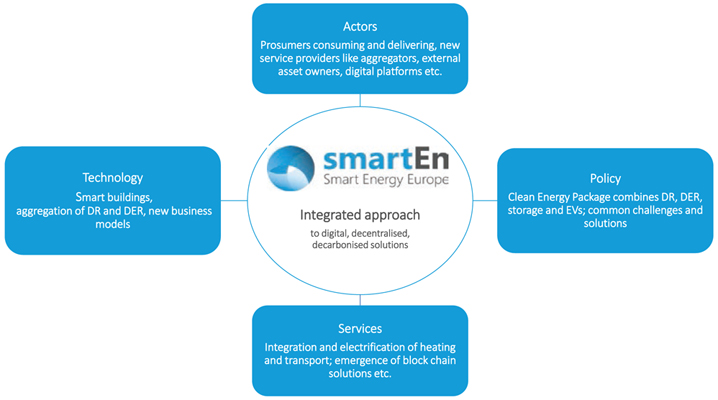

On the technology side, we see

decentralised generation go along

not only with the rapid evolution of

storage technologies, but also the

automation of devices, allowing for

demand response and technology

interaction at various levels.

The integration and increasing

electrification of transport and

heating, so called 'sector coupling', is

advancing. Automotive manufacturers

are cooperating or even integrating

with heating and solar companies to

promote interactive solutions. Smart

appliances and building automation

optimise consumers' energy use,

offering both comfort and the ability to

adjust to signals from the grid.

Services have moved beyond simple

supply. Digitally-enabled business

models have emerged from the

need for facilitation, aggregation and

market-placement of energy and

services from distributed resources.

For example, companies specialise

in the identification of flexibility

resources in large production sites,

helping consumers make use of their

potentials. Others provide residential

energy users with solutions to optimise

their local power production or the use

of their heat pump. Many of the service

providers themselves make use of

digital service platforms enabling their

business.

Coupled with this, the roles of the

different actors can no longer be

classified as they were. While network

operation remains a contained role,

the distinction between generators,

suppliers and consumers has

given way to new concepts and

combinations. Consumers are

becoming generators, asset owners

may be individuals, communities

or pension funds, and new service

providers have entered the market.

We are seeing traditional energy

companies with previous portfolios

of coal or gas generation, selling

off their assets and investing in

the management of decentralised

solutions and services. New market

entrants like independent aggregators

are establishing themselves as

important players, and traditional

manufacturing, telecommunications

and IT companies are entering the

energy space.

With the changing realities of the

energy system, regulation must also

adapt. Decentralised solutions are

a central part of the Clean Energy

Package currently under negotiation

in Brussels. An updated market

design that enables the efficient

uptake of demand response, storage

and distributed generation is on the

table, including proposals to open

the markets for innovative products

and service providers. For example,

consumers should have the right to

choose dynamic pricing offers or

engage in self-generation, buildings

should become smarter and be

certified as such, aggregators should

be given non-discriminatory conditions

to provide their services to consumers,

and distribution system operators

are encouraged to source efficient

flexibility services from the market.

NOW, WHAT DOES THIS MEAN FOR THE STRUCTURE OF THE ENERGY SYSTEM?

Is the top-down approach to the

energy system now giving way to a

bottom-up approach? Some current

trends suggest so. Driven by existing

market rules and incentive structures

that are heavily determined by the

blunting effects of rigid taxes, levies

and charges, many prosumers

using the new opportunities of selfgeneration

and on-site flexibilities,

choose to go off-grid or minimise

interaction with the system, rather than participating proactively. But

make no mistake! Decentralisation

does not require fragmentation

and autonomisation. A sustainable,

decentralised energy system will

build on an integrated perspective:

Consumers, prosumers and asset

owners should be able to use and sell

their energy and flexibility resources

wherever they are most valuable at any

moment. This means moving beyond

silos of demand or supply, locallevel

or system-level optimisation of

resources. In such integrated markets,

distributed energy and flexibility

supplies and services could be used

at every level and purchased by all

different actors – Distribution System

Operators, Transmission System

Operators, and all market participants.

For this to succeed, markets and

products must be streamlined between

the local and regional level, between

the provision of services for system

operation and energy for supplies.

The creation of a smart integrated

system also means that taxes, levies

and grid-charges must be revisited,

encouraging smart interaction rather

than pushing users away from the

system. If, in many European countries,

over two-thirds of a consumer’s energy

bill consists of flat taxes, levies and

charges that are based on the kilowatthours

consumed, grid defection is

a natural reaction. Different options

should be explored to overcome this

effect. Levies could be linked to the

point of fuel consumption, rather than

final electricity; dynamic taxes linked

with the electricity market price should

be assessed; VAT, which has been

linked with the volumes of electricity,

could instead be based on purchasing

price. Finally, if users can earn back

part of their network charges or benefit

by selling services to the system,

monetising their energy and flexibility,

they will tend to remain connected,

contributing to a sustainable, costeffective

and increasingly decentralised

energy system.

In this context, digital solutions will not

only support the provision of services

to the system, but they are essential

also for the operation of markets and

platforms. The market integration

and evolution of new and innovative

products on the power exchanges

and the trialling of new approaches

to service acquisition by Transmission

and Distribution System Operators

gives reason to be optimistic for the

next steps.

In an increasingly decentralised,

decarbonised energy system, we

need the digitally enabled interaction

of millions of demand and supply

assets and solutions. This requires an

integrated perspective - and this why

the Smart Energy Demand Coalition,

SEDC has become Smart Energy

Europe, smartEn.